When planning for retirement, most federal employees think about their own income—but it’s just as important to consider what happens after they’re gone.

That’s where FERS survivor benefits come in.

If you’re married or have loved ones who depend on your pension, understanding these benefits is crucial. They’re not automatic. You must elect them at retirement, and the decision is permanent.

Let’s walk through what survivor benefits are, how they work, and why it’s essential to weigh your options before making a decision.

What Are FERS Survivor Benefits?

FERS survivor benefits provide a monthly income to your spouse if you pass away in retirement.

They’re funded by taking a small reduction in your monthly pension. In return, your spouse receives a portion of your annuity for the rest of their life—even after you’re gone.

The Three Main Options at Retirement

When you retire, you’ll choose one of the following:

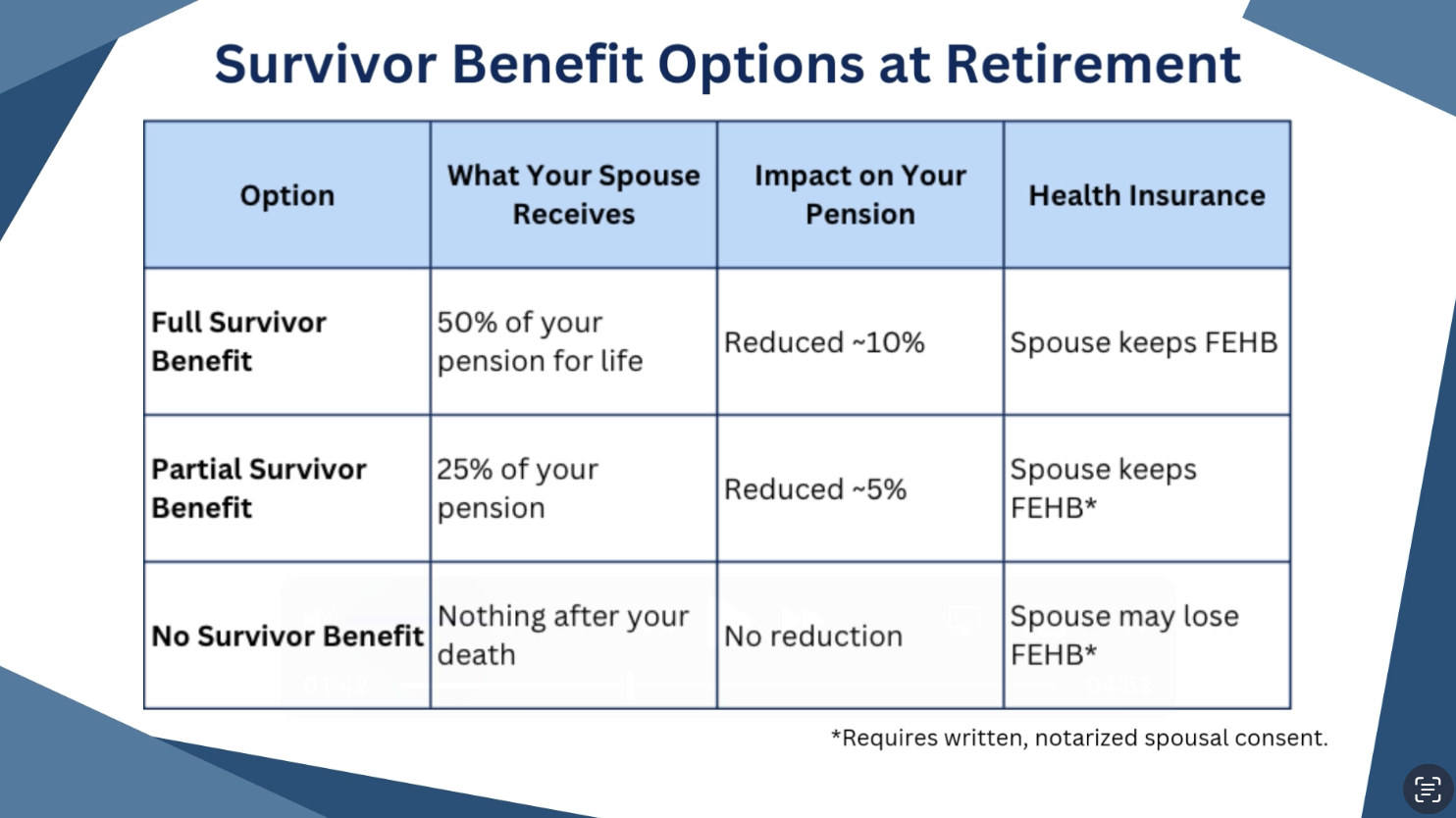

1. Full Survivor Benefit

- Your spouse receives 50% of your monthly pension for life

- Your pension is reduced by about 10%

2. Partial Survivor Benefit

- Your spouse receives 25% of your monthly pension

- Your pension is reduced by about 5%

3. No Survivor Benefit

- Your full pension is paid to you while you’re alive

- Your spouse receives nothing after you pass

- Requires written, notarized consent from your spouse

Why This Decision Matters

This isn’t just a checkbox—it’s a long-term income decision.

If your spouse is counting on your pension to help cover bills, housing, or healthcare, losing that income could be devastating. On the other hand, some retirees already have life insurance, other income sources, or a spouse with their own pension—so they may choose a different path.

The key is knowing what your numbers actually look like and how all the pieces fit together.

Common Questions We Hear

❓Can I change my survivor benefit election later?

No. Once your benefit election is made at retirement, it’s permanent in most cases.

❓Does my spouse lose the benefit if they remarry?

Not if they remarry after age 55. If they remarry before 55, the survivor benefit may be affected.

❓What happens if I choose no survivor benefit?

Your pension is higher while you’re alive, but nothing continues for your spouse. This also affects their eligibility for FEHB coverage after your death.

How We Can Help

At Independence Benefits, we walk you through your options in plain English. In your complimentary retirement session, we’ll:

- Go over your pension estimate

- Show you the exact impact of each survivor benefit choice

- Help you compare options using your actual numbers

- Coordinate your pension, TSP, and FEGLI decisions into one clear plan

- Answer all your questions—judgment-free and pressure-free

We’ve helped thousands of federal employees make these decisions with clarity and confidence.

Final Thoughts

FERS survivor benefits aren’t one-size-fits-all. The right choice depends on your personal finances, goals, and what kind of security you want to leave behind for your spouse.

If you’re within five years of retirement—or already retired and want a second opinion—we’re here to help.

💬 Book your complimentary retirement consultation today and let’s walk through your survivor options together.

FERS Survivor Benefits Explained: Protecting Your Spouse After Retirement :https://youtu.be/aTdb32ST20Q